高木 月人

株式会社ベネッセホールディングス

Digital Innovation Fund 全体運営

2010年サッポロビール入社。主にファイナンスや中長期経営計画立案などの経営戦略業務に従事。2016年より同ホールディングスのIR室長代理として年間150件以上の投資家対応を経験。約10年間の勤務で社長表彰など計3回受賞。

2019年よりGMO VenturePartnersの経営管理/財務マネージャーとして、投資先企業のモニタリングや支援業務、経営企画/財務IR/広報などを管掌。ケイマン諸島にて130億円規模のファンドレイジング。

2022年よりベネッセホールディングスにてDigital Innovation Fundの運営やスタートアップ投資に従事。

教育・介護領域のノウハウを活かした、グロース支援&シナジー創出で社会課題解決に繋げる

- ベネッセのDigital Innovation Fund(DIF)について教えてもらえますか。

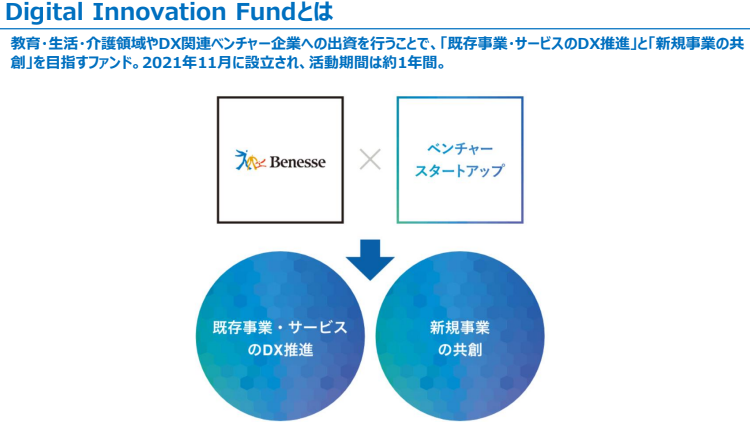

DIFは、教育・生活・介護領域やDX関連ベンチャー企業への出資を行うことで、「既存事業・サービスのDX推進」と「新規事業の共創」を目指しています。DIFメンバーは10名前後の体制で、基本的にグループ内のDX化を推進するBenesse Digital Innovation Partners (DIP)やベネッセホールディングス(HD)の財務部門などとの兼務となりますが、私のみDIFの運営及びキャピタリスト業務を専属で行う立ち位置になります。

DIPは、DX化を推進させるために、2021年春に作られた組織で、デジタル部門、IT部門、人事部門、DX推進のためのコンサル部門を統合したグループ横断型の組織です。グループ内におけるDX戦略の立案から資源・投資配分、具体的施策の推進まで、事業部門・会社の垣根を越えてDX推進を牽引する役割を担っています。

DIFはDIP設立から約半年後の2021年11月から活動を開始しました。

そのため、DIPの社内コンサルタントを兼務しているメンバーはコンサルティングファームからの中途入社組が多いですね。彼らは介護や教育などそれぞれの担当分野において、事業部門の経営課題にあたるDXプロジェクト案件を持っていて、それらを推進させるために寄与できるスタートアップとの協業をイメージしながら、DIFでのCVC活動に従事しています。また、DIFは他にもデータサイエンティストやデジタルマーケティング、VC、財務IR、広報ブランドディングなどバックグラウンドが多様な人財で構成されており、直近ではDeepTechに対応するため様々な技術に知見のあるメンバーをアサインしました。

私は唯一のベンチャーキャピタル出身者ということもあり、特に担当領域は持たず、横断的なポジションでソーシングやファンドの運営などに携わっています。

-DIFのファンドの概要を教えてください。

出資のスキームはHDからのBS出資です。組合形式での組成も議論をしていますが、CVCとしての主目的は協業などのストラテジックリターンであることを考えた場合、協業を推進する上では組合形式にする必要はないだろうというのが現時点での結論です。ただしストラテジックリターンがあれば良いということではなく、CVCとして外部LPが仮にいたとしても恥ずかしくない財務リターンを創出していくべきと考えています。

検討する場合のステージは、シードよりもシリーズA、B以降がメインです。

案件の属性によってはM&Aの部門に繋げることもあります。M&A部門とは常時連携をしているわけではありませんが、双方で相談を持ちかけることもありますね。ベネッセの介護事業は比較的後発でしたが、今では1200億円規模に成長しました。塾の領域もM&Aで拡大してきた歴史がありますし、比較的M&Aを上手く使ってきたグループだと思っています。

- DIFの投資方針であったり、「ベネッセがなぜスタートアップ投資を行うのか」という点について教えてください。

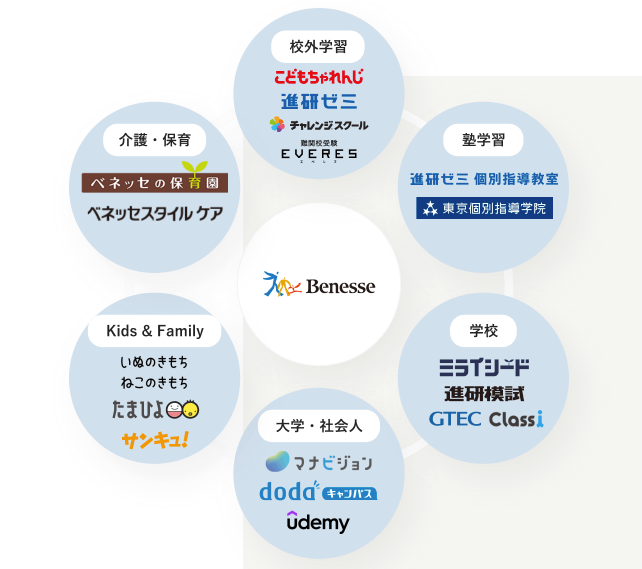

ベネッセという言葉は「よく生きる」という意味。ビジネスとして展開している領域も、「家族(キッズ&ファミリー)」、「学び(学校、塾、通信教育、スキル、資格)」、「生活(介護)」といった、人の営みと切っても切れない領域です。

事業をおこなっていく中で、多くの会社さんと競合しながら取り組んでいますが、こういった領域は一つの会社で幸福や変革を実現していけるものでもないので、競合しながらもその一方で、他社とも一緒にやっていこうという意志が当社には元々あります。

テクノロジーが進化し、若い起業家が社会変革に挑戦する世の中になってきたなかで、一緒にやっていこうという相手がスタートアップ企業になってきたので、そのHowとしてCVCが選択肢になったということと思っています。

その上で、CVC活動を通じての目的としては大きく次の3つがあります。

- コア領域での事業価値向上

- →教育などの当社コア事業の価値向上に資する投資で、スタートアップのグロースにも寄与できるもの

- 未開拓領域での協創関係

- →当社が保有しているが使いきれてないリソース(事業ノウハウ、顧客接点)をスタートアップが使い倒すことでスタートアップ側が成長し、当社がタッチできてない市場にアプローチができるという関係が築けるもの

- ベネッセのDX化推進

- →当社のインフラやシステムに、スタートアップのサービスを入れることで、当社がDX化の果実を得れて、スタートアップは売上やユースケースを獲得できるもの

事業提携自体は、出資をしなくても実現できますが、1回の提携や協業ではなく、資本関係を持って繋がりを作れる座組みとでは、やはり関係の濃さが違うと思います。上辺だけの提携になってしまっては意味がないですし。

ただ、デューディリジェンス(DD)は、純投資としてフィナンシャルなリターンが見込めるかと、ビジネスとしての協業が実現できるかを同時にしっかりみて、純出資として難しいという判断であれば、出資はなしで、まずは事業提携だけでの検討という話になることも多いです。

一方で、事業サイドでのシナジーがほぼ見込めないが、純投資的には魅力的、という評価になったとしても、投資は行わないという判断になるのが基本です。将来的に事業面で組めそうなら、純投資扱いで少額出資ということは検討できるケースもありますが。

VCではないので、投資ポートフォリオ的に、横断的な分野に投資をしておいてリスク分散をする、というやり方は、今のところは積極的には採用していません。

出資後の活動について教えてください。

CVCとして財務的なモニタリングを行いながら、事業部側が直接協業案件をハンドリングして動かしていくというケース、社内DXシナリオの場合は、対象となる事業部だけでなくDIPを兼務するメンバーが加わってスタートアップとPDCAを回していくケースもあります。また、当社のメンバー個人が出向レベルでスタートアップに深く入り、スタートアップ側の視点で案件を進めるという場合などもあります。

シナジー創出を目的とした投資が前提ですので、DIFのメンバーに限らず、協業にコミットするメンバーは、期待したシナジーが実現できているかについて、定量的に評価される仕組みが整備されています。例えば、事業の売上増や、事業部のコスト削減効果などですね。

- ファンドとして掲げる目標はありますか?

5年で50億円の投資という目安については発表している通りですが、だからといって、無理やり年間何件投資しなくてはいけない、というものをもって運営しているわけではありません。DIFはCDXO、CFO直轄チームということもあり、本当に魅力的な案件であれば、DIFという枠を超えて、M&Aチームとの協働も可能ですし、外部資金をいれているファンドではないため、方針も柔軟に変更可能で機動的に動ける組織です。だからこそ、1件1件、案件を見て判断していく運営方針を実行できていると思います。

- ベネッセのCVCとして独自の強み、面白みなどはありますか。

やはりベースに教育・介護系の事業を持っていて、この領域に関しては日本でトップクラスのノウハウや人財が社内に蓄積されていることが挙げられると思います。他のVCやCVCでは出来ないグロース支援、シナジー創出が可能だと思います。また、投資先のイグジットについて、多様に考え対処できるところはあります。例えば、既述の3つの投資シナリオのうち、3つめの、社内DX促進目的でプロジェクト的に資本提携をした先は、どこかの時期で投資回収を考えますが、1のコア事業の価値向上を目的で投資を行った場合、協業による価値向上がうまくいっていれば、スタートアップの上場後でも株を手放す必要はないですよね。ファンドではないので期限はないですし、事業と財務目線をそれぞれ考えながらケースバイケースでイグジットと時期をアレンジすることが可能です。

ベネッセの事業領域は、学びや暮らしなど、社会課題に直結するものが多い。そこの課題解決に資するような投資先と関係者全員でwin-winの関係を築くことで、ハードルは高いですが、大きな話でいえば、日本そのものをより良くしていくポテンシャルもあるように思います。

事業のないVCではできない取り組みができている実感があり、やりがいを感じています。

一方で、上場企業という社会の公器であり、VCのようにスタートアップ投資を目的とした投資家から資金を預かっているわけではないので、上場企業としてどのような投資が適切かという点は常に熟考すべきと考えています。

VCのように少額投資を可能性のある領域に分散投資するやり方はCVCでは難しいですが、手法としては魅力的ですし、CVCならではの投資のポートフォリオについては今後突き詰めて考えていく必要があると思っています。

そうやって考えていくと、CVCキャピタリストというのは投資家の目線、上場企業のビジネスパーソンとしての目線、起業家の立場に立った目線、色々な視点を使い分けながら全方位外交のような活動が求められる特殊な仕事なのかなとも思います。

それと、将来的にはBS出資を前提としているCVCも、ファンドとしてマネタイズできるようにしていくことも視野にいれるべきだと、個人的には思います。ファンドの組成はメリットデメリットがあるので、実際にやるやらないは目的に合わせるとしても、CVCをやる以上は、外部資金を入れて有期限でも成り立つファイナンシャルリターンを創出し、管理のケイパビリティを含めて持つことをイメージしておくことは意味があると思っていますし、自分も含め対応できるように能力を上げていきたいという思いもあります。

「ギアには遊びが必要だ、でなければ摩耗してしまう」

- 高木さんのお子さんの頃について話を伺って良いでしょうか?

私は東京の国分寺あたり、中央線沿いで生まれ育ちました。小さい頃は変わっていると言われていましたね。給食の時間が過ぎてまわりがボール遊びをしていても、ど真ん中で平気で一人ご飯を食べていられるような子供だったので(笑)。学校での勉強は嫌いで、屋上にばかりいるような子供でした。でも本を読むのが好きで、いくつかのマイブームがあり、ある時は心理学にハマったり、ある時は植物学、量子力学にハマってなど、そういう時期はその手の本ばかりを読んで、授業中に「こんな世界があるのか」と夢中になって読んでいました。

美術系も好きで美術史や、宗教学など世界の神話にも興味をもっていました。

母親は美大出身で、絵を描いたりカフェで歌を歌っているような人で、世間のことは知りませんというタイプ。父親はレコードの針の部分や補聴器などを作っていた音響系のエンジニアで、家でジャズを聴きながらプラモデルを作っていたような人です。両親に限らず、家系をさかのぼっても、モノづくりやクリエイターぽい人はいるんですが、企業に属したビジネスパーソンというのは私一人かもしれない、というような家庭環境です(笑)

なので、モノとか、美術品とかに小さい時からすごく興味があって、大学の時は時計を分解してずっと遊んでいました。

父親はお金を嫌うような古い考え方を持っているところがあって、そういう頑固なところはカッコいいなと思いながらも、世の中は資本主義で回っているとも理解していて。世の中の常識に適応しようとしない姿勢は損だなあとも思っていました。

大学はとにかく家が近くて無理しなくても合格できるところ、という今考えるとろくでもない考え方で選んだのですが、学部は経済学部を選んだり、社会人になって財務の仕事をしたり、という選択はお金があまり好きではないからこそ、お金に振り回されないために選択したんじゃないかと今は思っています。

高校時代はバスケ部に所属していましたがいわゆる幽霊部員で、楽しいときだけ顔を出すタイプでした。いわゆる「勝ち」に最後までこだわる気持ちが生まれなくて。なんで勝たなければいけないんだろうと本当に思っていました・・。自分や仲間がいいプレーをしたら楽しいし、そのことに集中してやっていましたね。

- 最初の就職先はどうやって決めたのですか。

ずっとものづくりをしている親の元で育ったので、何かしら手触り感のある事業を志向していて、メーカーを受けていました。加えて、扱っている商材が、人の気持ちが盛り上がるものが良いなと。

大学4年間はずっと居酒屋でバイトをしていて、店長代理みたいなこともやっていました。お酒を飲むこと自体は別に好きではなかったのですが、4年間で数えきれない数のテーブルを見てきて、最初は硬い雰囲気の人たちがお酒を介して和やかになっていくのをずっと見ていたので、ギアの潤滑油のような力を持っているお酒の魅力に惹かれていました。

小さな頃から宗教学や歴史は好きで、紀元前の話とかも大好きなんですが、お酒ってそんな大昔から人間の世界に寄り添っているんですよね。ウマル・ハイヤームという好きなペルシャの詩人がいるのですが、その人はひたすらお酒の詩ばかりを詠っているんですよ。人間は何かに酔っぱらっていないと生きていけない。(笑)

自分の中で相反する思想があって、ベジャンという熱力学者のコンストラクタル法則というものは、「生物・無生物を問わずすべてはより少ないエネルギーで効率的に流れが改善される方向にデザインされていく」という考え方があり、世界の流れがどんどん加速していくのは自然だし、流れに沿ってそれを後押しすべきだという思想を自分は持っています。一方で、加速だけしていく世界はどんどんつまらなくなっていくし、べたべたの非効率な人間的要素を愛している自分もいます。「ギアには遊びが必要だ、でなければ摩耗してしまう」という父の言葉が結構好きなんです。それがアナログなお酒の業界を選んだ理由と、今CVCキャピタリストという世の中を加速させる職業をしている背景にあるように思います。

- サッポロビール入社後はどういう仕事をされたのですか?

新卒のときから一貫して経理、経営戦略系のキャリアを歩むことになりました。

希望すれば他の部署にもいけたと思うのですが、財務系の仕事は数字という共通言語で、いろんな人と会話ができること、わかりやすい指標があるのでサポートもしやすいのがいいなと。最前線で剣を振るうより、盤面を見て全体最適を考えるほうが性に合っているので、そういった意味でも財務系の仕事は相性が良かったように思います。

ビール会社の人財を見ると、優秀なマーケッター、セールス、醸造家という方々はたくさんいるんですが、ファイナンスに強い方は多くないなと。そういう意味で他の人と差別化ができる、という視点もあって、入社して10年間、一環してファイナンス関連の仕事から離れませんでした。

また、会社の雰囲気がとても自分に合っていてよかったです。マイクロマネジメントのように縛られるのが好きではなくて、経営変革やセールスマーケ、人事、ブランディングのプロジェクトなど、様々なプロジェクトに関わりました。上司も私が何をやっているのか把握しきれてなかったと思います(笑)。

同期でMBAの勉強会を作って、高単価のものを少ロットで作って売り上げを積み上げるマーケティングのやり方を提案するなど、本気で遊ぶ感じで働いていました。

- GMOグループへの転職はどういうきっかけだったのでしょうか?

お酒の業界は10年スパンで変化していく世界。ワインブームや日本酒ブームなど、おおよそ10年単位でサイクルが回っているんですね。会社も仕事も大好きだった一方で、10年いて、いろいろプロジェクトに携わっていくなかで、既視感にみまわれるようになってきました。

IRを3年ほどやっていた頃、海外の機関投資家やアナリストとのやりとりで、日本という国に対するディスカウントを強く感じることがありました。

すごくネガティブに見られていると知って、日本の価値を上げるために何かできないかと、自分なりに情報収集して思ったのは、日本のスタートアップ環境の弱さでした。海外と比べて資金調達の額が桁違いに低い。産業の新陳代謝をするための、新しい細胞を生み出す環境が弱すぎることにショックを受けました。

新しい細胞を生み出すためには、その分野に投資をしていく必要があると思いましたが、投資の専門家や機能が社内になかった。

企業投資を学ぶという意味では、PEや企業再生系も頭をよぎりましたが、新しい細胞を生み出すことに関わりたいという思いが強く、事業会社での経験を活かせる場所として、CVCに転職しようと思いました。

経験がないのでキャピタリストど真ん中の仕事は難しいと思い、たまたまキャピタリストとバックオフィスの間のポジションでの募集があったGMOに応募しました。

- それまでのキャリアと世界観が全く違う業界に転職し、当初はどんな感覚でしたか?

入社して初めは用語も出会う人々も視点も違うので、とにかく新鮮でした。業務としては投資先のモニタリングや間接的な支援から、ファンドレイズやCVC運営会社の財務や広報、人事総務、法務関係などファンドマネジメント全般の業務に関わりました。

この世界はファジーだから、ダイバーシティが必要

-GMOでも幅広い業務に携わる中、ベネッセへ転職のきっかけはどういうものだったのでしょうか?

投資やファンドマネジメントを学ぶための修行という気持ちでいたので、本音を言えばそんなに長くは勤めないだろうなとはどこかで思っていて、転職活動を始めていました。

自分はどういう領域に進みたいんだろうと考えている時に、27歳ごろの体験を思い出したんです。サッポロビール時代の話ですが、上司の紹介でロータリークラブの下部組織の活動を手伝っていて、会長や国際奉仕委員長という立場でネパールのボランティア活動に4年ほど従事しました。現地への寄付から始まり、インフラの整備や給食支援、絵画コンテストの企画など様々な活動に発展していきました。

ネパールはカースト制度が色濃く残っていて、人権を保証されていない子供達、教育を受けられない子供たちがたくさんいます。活動を通して、子供たちが感動している姿が心に強く焼き付いていて、とても充実感があったなぁと。

そんな原体験を思い出しながら、転職活動をしていたら、たまたまベネッセから連絡がきたんです。教育や人の生活を支える会社からのCVCの話。

これは「ドンピシャ」だと思い、転職したのが昨年の10月です。

- ベネッセにおけるDIFのキャピタリストとしてのキャリアをどう考えていますか?やりたい仕事のイメージなど教えてください。

”スフマート”という、ダヴィンチが完成させた、輪郭をぼやかす技法があるんですが、私は性格的に窮屈なのは嫌なので、スフマートのような、輪郭のない働き方が好きですね。転職した今もサッポロビールやGMOなどの仕事を有償無償問わず手伝っていますし、複数のスタートアップにも、アドバイザリーのような形で関わっていて、ベネッセという会社は自分がやるべきだと思ったアクションを自由にやらせてもらえる懐の深い会社だなと思っています。

スフマート(イタリア語:Sfumato)は、深み、ボリュームや形状の認識を造り出すため、色彩の透明な層を上塗りする絵画の技法。特に、色彩の移り変わりが認識できない程に僅かな色の混合を指す。レオナルド・ダ・ヴィンチ(1452年 - 1519年)ほか16世紀の画家が創始したとされる[1]。

そんな感じなので、私には起業家のように一つのことに強烈な、ある種エゴ的な情熱を燃やすことはできないですが、支援する役割を担うことはできるはずとも思っています。どうせ仕事をするなら、自分ができないことをやっている人たちを支援できる立場で取り組みたいですし、やはり、新しい事業なり産業なりを作っていくことには挑戦したいと思います。

「学び」を扱うベネッセという観点では、資本主義というゲームのルールを社会人にならないと学べないのではなく、もっと早期に教えるような取り組みができたら面白いと思っています。やはり父親の姿を見てきましたし、経済合理性だけを追求する世界はつまらないと考えているので、だからこそ、well Beingに繋がるやるべきこと、やりたいことをやるためにも、経済を冷静に捉えられる感覚を小さい頃から養う機会を提供できないかなと思っています。

- どんな起業家やキャピタリストと会っていきたいですか?

こういう人にだけ会いたいということはなく、どんな人にでも会いたいなと。単純にお金を稼ぎたい、有名になりたいというモチベーションの方でも、社会課題に取り組みたい方でも。

CVCキャピタリストとしての視点でいうと、自論としてIRや広報を軽視する起業家にはネガティブです。スタートアップはしっかりした中身がまだないなかで、「見せ方」は想像以上に重要なファクターです。それがしっかりしていれば、周囲を巻き込むことであらゆるリソースが後からついてくる。本質ではないと思われるかもしれませんが、私の専門性がIRにあるということもあって、極めて重視しています。IR広報でストーリーを戦略的に周知していって、それを確実に達成した姿をまたIRしていくことができる会社は、極めて高い確率で強い会社になっていくと確信しています。

- 最後に、CVCキャピタリストという仕事についてのご意見や、メッセージをお願いします

キャピタリストに外国人がもっと増えたらいいなと思います。日本と海外ではUI/UXなどの好みは異なります。海外で当たったものは作り直さずすぐにグローバル展開できるので、そういった投資または支援ができるキャピタリストがいたらいいと思います。ダイバーシティインクルージョンが流行りだから言っているのではなく、やはりいろんな人達がこの業界に流れてきた方が面白いし、スタートアップは未来を形作るわけですから、偏った人たちがその支援をしたら、偏った方向にいってしまうかもしれない。白も黒もないし、すべてがスフマートのようなファジーな世界において、絶妙なバランスをとっていく必要があると思うんです。だから色んな方向に尖った人たちが集まることで、結果的に調和のとれた未来が形作られていくんじゃないかと思っています。