竹川 祐也 / Yuya Takegawa

サイバーエージェント・キャピタル

取締役 パートナー

証券会社、人材紹介会社を経て、2004年よりベンチャー投資活動に従事しフルスピード、ライトアップ、ステムセル研究所、セイファート等のスタートアップ12社へ出資。2007年デジタルマーケティング支援を行うITベンチャー企業ノッキングオンに入社し翌年CFOに就任、事業会社による買収を経て2010年にCEOに就任。2012年11月サイバーエージェント・キャピタルに入社。2014年12月にシード特化型ファンドSeed Generator Fundを立ち上げライボ、PETOKOTO、バックテック、Gozal等の創業期のスタートアップ15社に出資するなど主にシード期の起業家に対しての投資活動を行っている。早稲田大学文学部卒。趣味は草野球。

起業家ファーストで、シード投資にこだわる

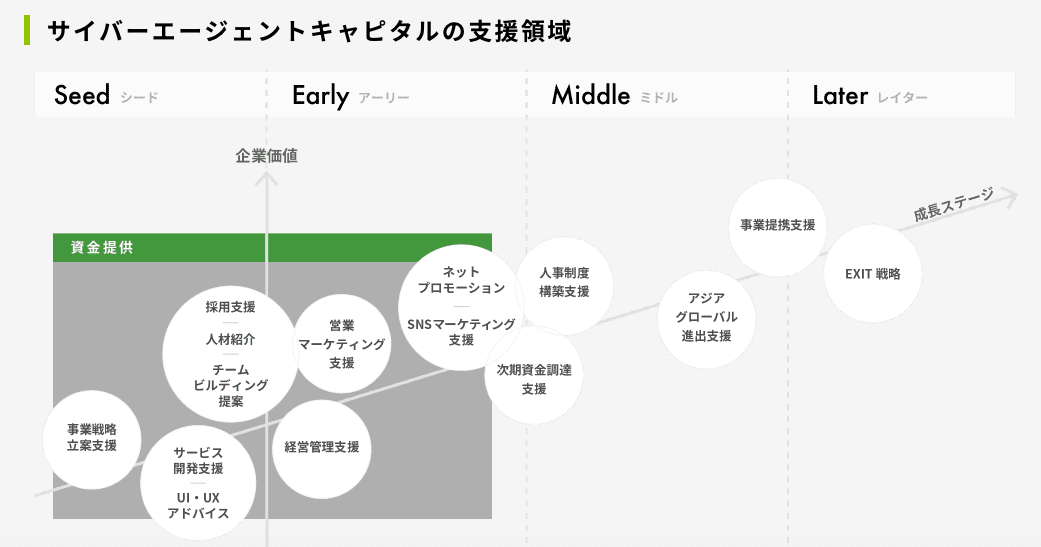

- 竹川さんが所属されているCyberAgent Capital(CA キャピタル)の投資領域やストラクチャ、組織などについて教えていただけますか?

CAキャピタルは2006年に設立され、現在は60億円規模の3号ファンドを運営しています。投資ステージは主にシードに注力しています。親会社でありメインの出資者であるサイバーエージェント(CA)はインターネット広告、メディア、ゲーム、投資育成等の事業を行っており、投資対象の領域は、知見が活かせるという意味でインターネット、IT関連が中心となっています。

出資者についてはCAがメインとなりますが、CA本体とのシナジーや、M&Aといった戦略的な目的での投資をするためだけのファンドという建て付けではありません。

ですので、意思決定については純投資に近い考え方で臨んでいます。例えば、CAが行っている事業と競合している事業であっても投資検討が可能です。

拠点としては、日本以外にも、アメリカ、中国、インドネシア、タイ、ベトナムにも拠点があり現地の起業家・投資家のコミュニティに入りながら投資活動を行っており、現在日本で100社以上、海外含めると200社以上のスタートアップに投資をしています。

日本チームは代表の近藤ほかメンバー10名ほどの体制です。シードやアーリーステージのスタートアップの成長のお手伝いをするため、チームにはキャピタリスト以外に、CA本体で実務を経験した、技術や採用、広報などの支援を担当するメンバーがおり、グロースチームとして投資先の支援を行っています。

- 親会社とのシナジーを最優先とはしないCVCは珍しいと思います。どういう思いが込められているのでしょうか。

全く連携しない、というと言い過ぎかもしれません。我々が最もCA本体との距離感が近いですから。純投資でありながら、連携の機会も追求する、というちょっとずるいスタンスです(笑)。起業家、創業者の皆さんが求める限りにおいて、そしてお互いにフェアにビジネスができる前提で、本体に最も近い我々が適切な部署や担当にお繋ぎする動きもしています。ただ、連携そのものを前提には投資しないということです。このあたりの考え方は、そもそもの投資事業の成り立ちとして、CA自身がベンチャー企業としてその道程を歩んできたこと、社内でも多くの新規事業の立ち上げに挑戦してきたこと、という背景から、起業家の立場で考えるというカルチャーが存在することが大きいと思います。主役である起業家の思いを汲み取り、CAのように挑戦し続けるベンチャー企業、スタートアップを増やしたい、ということかと思います。

当社の中では「起業家ファースト」という言葉がよく使われます。起業家の目線に立った時、最も重要なのは我々の親会社とのシナジーではなく、スタートアップ自身の事業の成長です。出資後、必要な際は助言やリソースを提供するなど一定の関与は行いますが、あくまで重要な経営判断や実行、組織づくりの方向性など現場は起業家や経営チームが担います。多くの事例を見ているからこそスタートアップの主体である起業家やチームへのリスペクトを忘れないことが大事です。それが「起業家ファースト」であるべきという、CAキャピタルの考え方です。

CAキャピタルでは、これまで実際に事業に深く携わったことがあるキャピタリストが多く在籍してきており、その経験もシェアされ引き継がれています。事業を立上げPMFを目指すシード期や、アクセルを踏んでスケールを目指していくアーリー期以降のスタートアップをサポートしていくのに求められるのは、投資の経験だけでなく、事業の現場を理解し当事者の気持ちに寄り添うスタンスが必要だと思っています。

起業して事業をすぐに成長軌道に乗せることは簡単ではありませんし、全員が成功するわけでもありません。繰り返しになりますが、CAはベンチャー企業として、これから成長するスタートアップよりも少しだけ先に進んでいるのかもしれないですが、新しい力で世の中を前向きに変革する仲間として、同じ価値観を共有するベンチャー企業として、同じ目線でスタートアップを支援していくという姿勢は、今後もCAキャピタルとして大事にしていきたいと思っています。

-実際の投資活動について教えていただけますか?

投資委員会は基本的には週次で開催しているため、早ければファーストコンタクトから2-3週間で投資の意思決定ができます。また、キャピタリスト毎にカバーする事業領域を分けてはおらず、それぞれが興味関心を持った領域について深掘りながら、お互いの知見をシェアしながら議論を進めていきます。たとえば今なら生成AIなどの関心領域のスタートアップにどうアクセスするかなどトレンドのテーマに対しても議論する場は常に設けていますし、海外の動向をリアルタイムで把握するために全キャピタリストが集まるオンラインのグローバルミーティングも月に1回開催しています。

いわゆるシードラウンドが中心ですので、幅はありますので目安に過ぎませんが1件あたりの投資金額としては2,000〜3,000万円、バリュエーションでは2〜3億円くらいが平均的なレンジかと思います。

出資時のスタンスとしては、スタートアップにとっての最初の投資家、且つそのシードラウンドのリード投資家となることをイメージしています。

なおリード投資だとしても、要請がない限りは取締役等にはなるケースは少なく、経営会議や取締役会などの機関にはオブザーバーとして出席するにとどめるケースが多いです。もちろん経営を左右する機関決定は大事なのですが、シード期はまずPMFを達成するところにフォーカスすべきなので形にこだわらず機動的にコミュニケーションを行うことを重要視しています。

-シードラウンドとなると、いわゆるPMF(プロダクトマーケットフィット)を迎えていないスタートアップへの投資になります。まだプロダクトが完成していない段階で、何を見て投資判断を行っているのでしょうか。

一概に「これが大切」ということを言うのは難しいですが、ファウンダーマーケットフィットは重視するポイントです。

創業者が、その領域でチャレンジする理由があるか、領域におけるユーザーインサイトが誰よりも深いか、と言う点です。また、事業や会社をスケールさせるために必要なチームビルディングができるか、採用力があるか、について、過去の経験や、人との接し方、巻き込み方などを見ています。そこに繋がる部分もあると思いますが、会社や事業の方向性を魅力的に語れるか、言語化できるか、困難に遭遇したときに遠慮なく周りを頼れるか、失敗からの学習スピードが速いかという面も見ていきます。

経験を積むことで成長、変化していく部分もありますが、人の生来の性格に根差したような部分は良くも悪くも変わりづらいと思います。なので、はじめての起業家と会話をする時は、その起業家がどのようなチームを創りうるのかということを想像しながらお話を伺っています。

さらにPMF後を見据えると、数字を意識した会話ができるかという点も重視しています。事業をスケールするフェーズでは、事業状況を定量的に把握しスピーディーに対処することが大切ですので、メッシュの細かさや精緻さに差はあったとしても、適切なKPIを設定・可視化し、それについての様々な角度から議論ができるか、そういった素地があるかには関心があります。

もちろん、事業成長の面では、いまは小さくともマーケットの奥行きがあるか、マーケットの成長を支えるシナリオが不可逆的なものか、既に大きなマーケットを新たなプロダクトでひっくり返せるかといったことも確認します。最も分かりやすい例で言えば、人口動態は変化しにくいわけで、高齢化や労働人口の減少をベースシナリオに据える市場は魅力的に見えます。その他、国策、規制緩和、新しい技術・デバイスの登場等、これからの市場の方向性を決め、かつ事業のスケールが期待できる条件がどれくらい揃っているかを見極めようとしています。

ITバブル崩壊とリーマンショック。二度の激変を目撃

- 竹川さんご自身は、どのような幼少期を過ごされたのですか?

出身は広島県広島市の元宇品町という小さな島でした。

先日G7の会場になったところです。通っていた小学校は全校100人くらい、1学年1クラス10人くらい、と自然に囲まれた本当に小さな学校でした。6年生で生徒会長を務めたりもしましたが、いま思えば随分生意気な小学生だったのではないでしょうか(笑)。習い事は止めそうになりながらも剣道を6年間続けました。

また小さい頃は読書が好きでした。きっかけは小学校入学のタイミングで祖母にプレゼントされたミヒャエル・エンデの「モモ」だったと思います。当時はまだゲームもインターネットもありませんし、テレビは親に占領されていますから、娯楽といえば読書でした。それをきっかけに色々な本を読むようになりました。高学年の頃は学校の図書室にあった江戸川乱歩や、シャーロックホームズシリーズなどの推理モノをよく読んでいた記憶があります。

中学/高校は家からも近かった大学の附属校に通いました。中学では野球に打ち込み、高校ではコピーバンドを組んだり、応援団で活動したりと、個性的で優秀な仲間に囲まれて、楽しく学校生活を送っていたように思います。いまはあまり会うことはできていませんが、各方面で活躍している当時の友人に刺激を受けることも多いです。

大学は早稲田の文学部に進みました。高校の時は興味があること以外は勉強していなかったので、受験をすると決めた段階では教師からは現役は厳しいのではと言われていましたが、自分の得意科目に絞り、戦略的に臨んだことで何とか無事に進学することができました。

- 社会人としてはどのようなキャリアを歩まれましたか?

大学時代は、スキークラブに入りました。スキーはそれほど上手くなりませんでしたが、3年生のときには300名規模の大会で実行委員長を務め、バックグラウンドが違う仲間たちとひとつのイベントを作り上げる喜びを体験しました。その後も青春を満喫していたら(笑)、2年も留年してしまいました。このときの仲間たちもいまだに繋がっていて刺激をもらっています。

就職するときは2年先に社会に出て活躍している同い年の友人に追いつくには、小さい組織に入って成果を出すのが近道かと思ったことと、どうせやるなら、興味が持てる領域でということで、スターフューチャーズ証券という証券業に新規参入した会社の証券部門一期生として入社しました。

学生時代、インターネットが一般的に普及し始め、ネット専業の証券会社が話題になった頃でした。株式投資にはもともと関心があり、新しい物好きでもあったので、ネット証券の口座をつくり投資信託などを購入していたこともあり、何となく証券会社が向いているようには感じていました。

入社後は、大手証券などで実績のある先輩たちに囲まれながら、会社経営者や医者といった富裕層のお客様に、電話をひたすらかける毎日。不幸中の幸いというか、投資信託の取扱がなかったため、個別銘柄を提案する必要があり、会社四季報などを見ながら、有望と思う銘柄を深掘りして、お客様に勧めていました。会社の情報を自分なりの切り口で分析/評価し、第三者に噛み砕いて表現をすることは、今のベンチャーキャピタリストとしての仕事につながるところがあると思います。

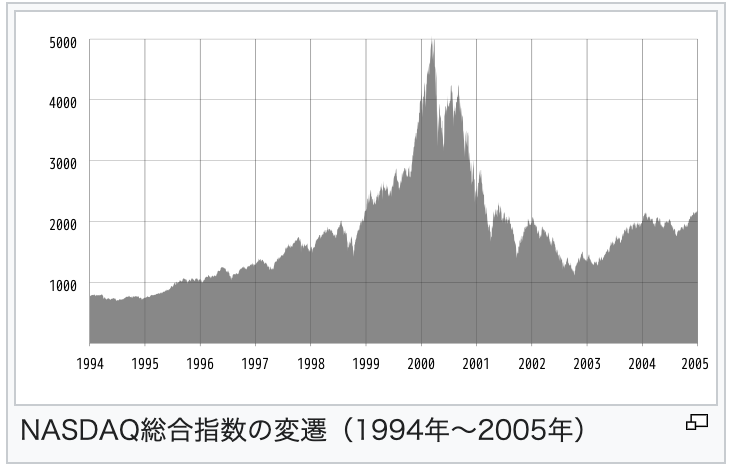

実は、私が社会人になった2000年はちょうどCAやライブドアが上場した年でした。仕事を通じて、次々と現れるベンチャー企業が高い株価でIPOを実現していくのを目の当たりにしました。そのなかで、徐々に自分自身もベンチャーに入って、大きなチャンスを掴む可能性に賭けたいと思うようになりました。

そこで、当時友人が勤めていた人材大手グッドウィルグループの人材紹介会社にキャリア相談をしに行きましたところ、「ウチもベンチャーだし、営業力は活かせるぞ、来ないか」と説明を受け、まさかのオファーに驚きながらも同社に転職することになりました(笑)。入社後、当時の代表含め主要メンバーの離脱等もあり、半年ほど経った後にその職場の先輩が立ち上げた別の人材紹介会社に事業立ち上げメンバーとして合流しました。

新興の人材紹介会社が、他社と差別化するためには魅力的な求人案件が不可欠。それを自分たちで作ろうと、ベンチャー企業に対して、成長ステージに合わせたCxO人材の採用を提案し、求職者をスカウトするというアイデアを実践しました。そのために自社で求人獲得の営業を行うだけでなく、ベンチャーキャピタル(VC)やプライベートエクイティ(PE)の現場の方々にコンタクトを取り投資先のCxO案件を投げて頂いていました。このような形で優秀な方をベンチャー企業のマネジメント層としてご紹介していくやり方は徐々に浸透していき事業も順調に成長しました。

一方で、VCやPEの人たちとの接点が増え、起業家の方々とも向き合っていくなかで、人材面だけでなく、資本面でも貢献する形でのベンチャー企業の支援がしたいと思い、次のキャリアを見直しました。そのなかで、未経験でベンチャー投資に携われるということで未来証券(現・みらい証券)という独立系証券に入社しました。JAFCO、日本アジア投資の2社で社長をつとめられた今原さんが3社目に立ち上げた会社で、JAFCO等のVC出身者の方が多数在籍されていました。

入社後は、証券や人材紹介の時代と同様、テレアポや飛び込みで、投資先候補となるベンチャー企業へコンタクトし、関係作りをし、先輩を引きずり回して仕事を学ぶ日々でした。IPOを控えたレイターの企業が主な投資対象だったので、データベースやメディアでそういう企業の情報を調べ、とにかく会いにいく。有望なベンチャーに投資するために、その企業の営業を手伝ったり、知り合いの人材を紹介したり、一緒に飲んだり、できることはなんでもやりながら、「自分たちが株主になるメリット」を作る、ということにフォーカスしていました。

そう言った苦労の甲斐もあってか、3年の在籍で12社へ投資をさせていただきました。マーケットはITバブルの崩壊から復帰するトレンドにあり、ポートフォリオの1社、フルスピード社は投資から1年ほどで上場し、大変良いパフォーマンスとなりました。同社にはCAキャピタルも投資をしていて、その縁で後に上司となる田島さんとも知り合いになりました。

未来証券の経験で、ベンチャー投資の仕事に魅了され、この仕事が天職と確信しました。起業家は前向きで、新しいことに挑戦している人たちです。彼らとのディスカッションによって知的好奇心が刺激されるだけでなく、「絶対うまくいくこと」「正解」がなく、常に新しい問いに向き合える面白味を感じていました。そして投資が成功した時は大きなリターンに繋がる。そういった新奇性とボラティリティの大きな仕事は自分の性格にも合っていました。

その一方、もっと起業家からの信頼を得る、ベンチャー企業経営者に向き合い続けていくためには、外から投資家として関わるという立場だけでなく、自らベンチャー経営の一部を担う経験を積むことが必要なのでは、と感じる場面も増えていきました。フルスピード社が上場したタイミングで、自分の中で気持ちが一区切りついた感覚もあり、旧知の仲だった創業者に誘われ、ノッキングオンというベンチャー企業に、2007年に経営企画室長として参画し、その後CFOという立場になりました。

同社は、当時アフィリエイト広告や販促プロモーションや、金融機関向けのデジタルマーケティングなどを提供する会社でした。参画時は30人ほどの規模で、業績も順調に伸ばしており、これからIPOの準備に入るというタイミングだったのですが、そのさなか2009年のリーマンショックの影響で主要事業の売上が急激に縮小。上場準備をストップし、主要事業を停止し、育成していた新規事業に注力し利益が見込めるまで組織をサイズダウンすることに。大きな方針転換の中で、創業者の意向もあり、某上場企業の傘下に入ることになりました。それに伴い創業メンバーが経営から離れたため、私がCEOという役割を引き継ぐことになりました。

前後して、この時期はガラケーからスマホへの過渡期で、次の柱となる事業の育成に悩みました。メディア事業を買収するなど新規事業に手を広げて再浮上のきっかけを模索していたのですが、利益は出るものの成長率という意味では満足いく結果を出すことができませんでした。結果として代表を引き継いで2年で親会社に統合する方針が決定され、2012年、私も同社を離れることになりました。

-市場の激変を二度も体感されたのですね。その後、CAキャピタルへ行かれたきっかけは何でしょうか?

当初は、もう一度ベンチャー企業CFOとして参画して、上場までやりきる挑戦をしようと思っていました。色々な知人に相談をし、実際にお声がけを頂けていた会社さんもあったのですが、最終的にはCAキャピタルの当時の代表の田島さんからの「有望なベンチャー1社にCFOとして行くのではなく、有望なベンチャー企業を100社生み出すキャピタリストにならないか」という言葉に心を動かされ、決断をしました。

最近は古株にもなり若手の育成にも当然関わりますし、業務の幅は広がってはいますが、基本的にはCAキャピタルの主軸であるシード投資を行うベンチャーキャピタリストとしての仕事に一貫して携わってきています。

同じスタートアップ向けの投資と言っても、未来証券でやっていたミドル・レイター投資と、シード投資とは考え方、捉え方が全く異なり、当初は自身の感覚をアップデートするのに苦労しましたが、社内外の方に揉んで頂いたおかげで、2-3年で地に足がついて活動できるようになっていったように思います。

シードステージでは、事業モデルすらまだ固まってないわけで、いかにユーザー感覚をもって仮説を立てるか、モックプロダクトに向き合うのか、起業家とのディスカッションで初期の問いを研ぎ澄ましていくのかが大事です。キャピタリストとしてどう起業家に良いインパクトを与えられるのか、もがいていた私に、田島さんからは愛ある厳しいご指導をいただくこともありました(笑)

ただ、CAらしさというか、メンバーと自由にディスカッションができ、お互いの悩み事やアイデア、ナレッジを共有し合えるフラットなコミュニケーションがしやすいカルチャーがあったおかげで、居心地の悪さを感じることは全くなく、それはいまも変わらない良さではないかと思っています。

その後、少しずつ信頼を頂いた結果でしょうか、2014年にはエンジェルラウンドに近いタイミングでスピーディーに投資を実行できる投資枠を立ち上げる試みにもチャレンジさせて頂くなど、色々なプロジェクトに関わりながらも、天職であるベンチャー投資の世界にどっぷり浸かりながらいままで仕事ができています。

起業家が始めなければ、投資はできない

- 竹川さんは、スタートアップ投資のキャピタリストという仕事をどう捉え、どのような気持ちで向き合っていますか?

投資判断のポイントは既述の通りですが、シードフェーズではプロダクトが未完成な分、起業家やマネジメントチームなど「人」を見て投資する比重が大きいです。

シードのスタートアップへの投資件数が増えても、一度投資実行に至った起業家やそのチームに対しては、最後まで味方として見守っていくという気持ちでいます。気づけば12年近くCAキャピタルにいるということは、投資した会社とシード期から苦楽を共にする喜びに取り憑かれているとも言えるのかもしれません。

仕事をする上で常に意識しているのは、事業創造のオリジネイターである起業家へのリスペクトです。どれだけVCにお金があっても、その資金を必要とする起業家が存在しなければこの仕事は成立しません。ベンチャーキャピタリストに限らずですが、お金を提供する側の立場は、ちょっとでも油断すると自尊心が肥大化しやすい立場だと思います。それゆえに、自分へ言い聞かせるだけでなく、若手メンバーに対しても、口を酸っぱくして「起業家ファースト」の意義を繰り返し伝えるようにしています。

- 竹川さんが考える、理想のキャピタリスト像や、ご自身の目標などがあれば教えてください。

CAキャピタルに入社したての頃は、シード期ということもあり、まずは起業家の人となりや創業チームの強さを見ることに集中して、投資後の事業成長と自分の当初の起業家やチームへの見立てとの関連性を検証し続けていました。これは私見ではありますが、キャピタリストとして、起業家の人となりや欲求の源泉を洞察し、事業成長と結びつけるという、ファウンダーマーケットフィットへの見立ては必須だと思います。また、一度投資を実行し「応援する」と判断したなら、求められる限り最後まで支援していく姿勢が大切だと思います。

VCファンドでは、投資先の起業家が上場等で得た資金から次のファンドへ出資していただくこともあります。もちろんファンドサイズにもよりますが、これは起業家とキャピタリストの一つの理想形かもしれないと私は思っています。

起業家に限らず、人と関係性を作って、その関係を尊重しながら物事を進めていくことが好きなので、信頼関係を大事にしながら、良い結果を出していくことにはこだわっていきたいと思っています。そして、すぐに結果が出ないシード期のスタートアップ投資だからこそ、何よりもまず私自身もこの仕事を「やり続けること」を意識しています。

- 近年、多くの事業会社がCVCを立ち上げるようになりました。長くCVC投資に取り組む立場から、CVCやCVCキャピタリストの課題や期待について伺えますか。

まず、CVCの増加については、スタートアップにとって、資金調達や事業連携など、成長につながる選択肢が増えたという面でポジティブです。以前は私にもCVC立ち上げのご相談を受けたことがありました。我々が純粋なCVCではないので、偉そうなことは言えませんが、過去の趨勢を振り返って感じたことでお伝えしていたのは、まずは「フロントには目立つ方を据えて、基本変えずにやっていくと良いですよ」ということでした。個人の顔が見えづらい大企業の中で、スタートアップ側に立って支援していく役割の人は、人事異動などもなく、基本ずっと変わらないくらいの方が良いと思います。

また、スタートアップの成長にコミットし、イノベーティブな事業を共創するということであれば、フォローでのマイノリティにとどまらず、財務リターンもしっかり確保する事や、リード投資や、M&Aなどの踏み込んだ取り組みにも挑戦することが良いと思います。

CVCからの出資をきっかけに、JVやM&Aなどに発展し、新しい事業創出に繋がったという好事例が、どんどん出てくると良いですよね。大企業にとっての新事業となると、ミニマムでも営業利益で数十〜数百億円に育たないと、という感覚かと思いますし、その期待にストレートに答えるとすると、マイノリティで出資して、成長してきたらM&AやJVも考える、というのではなく出資するからには自分たちがその規模まで育てることに主体的にコミットする、ということで良い成功事例が生まれてくるのではないかと思っています。

またこの数年で、岸田政権もスタートアップの育成に言及するなど、日本社会におけるスタートアップへの関心、注目度はかつてないほど上がっており、その中で、VC・CVCのキャピタリストが活躍できる場面も増えたと思います。

もし自分がキャピタリストという仕事に興味を持ったなら、本やこういったメディアで情報収集するのも良いですが、何よりも人に会って直接お話を聞くのがおすすめです。知り合いの起業家に、「好きなキャピタリストは誰か」を聞き、その理由などを深掘ってみるなど、数をこなせば、かなりの学びがあるはず。会いたいと思ったら会いにいく知的好奇心で動かされる人、面倒くさがらず1次情報を取りにいける人が、キャピタリストに向いていると思います。もちろん1次情報に触れていなくても類推してそれっぽい話ができるという方も居ます。これも一つの優秀さだとは思いますが、特にシード期、ユーザー候補と向き合いながら改善を繰り返すPMF前後の起業家に寄り添うベンチャーキャピタリストとして、少し勿体ないかなとも思います。

- 最後に、キャピタリストの仕事を通じ、竹川さんが実現したいことについてお聞かせください。

スタートアップの世界は、変化していくのが常。これからも、新しい起業家の出現と共に新しいビジネスチャンスが次々に生まれていきます。そんな中で、起業家が日々向き合っているさまざまな世の中の課題に、同じ目線で向き合い、問いを立てることを厭わないキャピタリストが増えてほしいし、自分もそうありたいと思います。

孤独のなかで、自分の思いや見立てを信じて、事業家としての道なき道を切り拓き、社会に新しい価値を生み出すための挑戦を続けるという「起業家精神」が、もっと社会の隅々にまで広まっていけば良いと思っています。私たちベンチャーキャピタリストが、起業家のヴィジョンの実現を支え、間接的にであっても「起業家精神」の布教の一部を担う職業として魅力的であると認知されていけば、自ずともっと世の中は良くなる、という思いを持ちながら、これからもこの仕事を続けていきたいと思います。