田口順一

三菱UFJキャピタル株式会社-投資第二部部長

1974年生まれ。早稲田大学商学部卒業後、デロイト・トーマツ・コンサルティング(現アビームコンサルティング)にて業務改善コンサルティングに従事。

2001年11月よりダイヤモンドキャピタル(現三菱UFJキャピタル)にてIT(製造・ソフトウェア)からサービス業まで幅広い領域のベンチャー企業への投資業務を20年以上に渡って手掛けるベテランキャピタリスト。

リーマンショック以降は、X-tech、メディア・コンテンツを中心にシードステージからレイターステージまで投資を行っている。

【主な担当投資先】

株式会社ホロラボ https://hololab.co.jp/株式会社Spider Labs https://jp.spideraf.com/株式会社AppBrew https://appbrew.io/株式会社トリビュー https://corp.tribeau.jp/株式会社ROXX https://roxx.co.jp/トリニティ・テクノロジー株式会社 https://trinity-tech.co.jp/株式会社VARK https://vark.co.jp/パラレル株式会社 https://www.parallelcorp.com/ファンズ株式会社 https://corp.funds.jp/

設立48年目のVCで、20年超のキャリア。

- 田口さんはキャピタリストとして20年以上、第一線で活躍されてらっしゃいます。その間、一貫して三菱UFJキャピタル(MUCAP)に所属されてらっしゃいますね。そのお立場から、まずはMUCAPの特徴と魅力について教えてください。

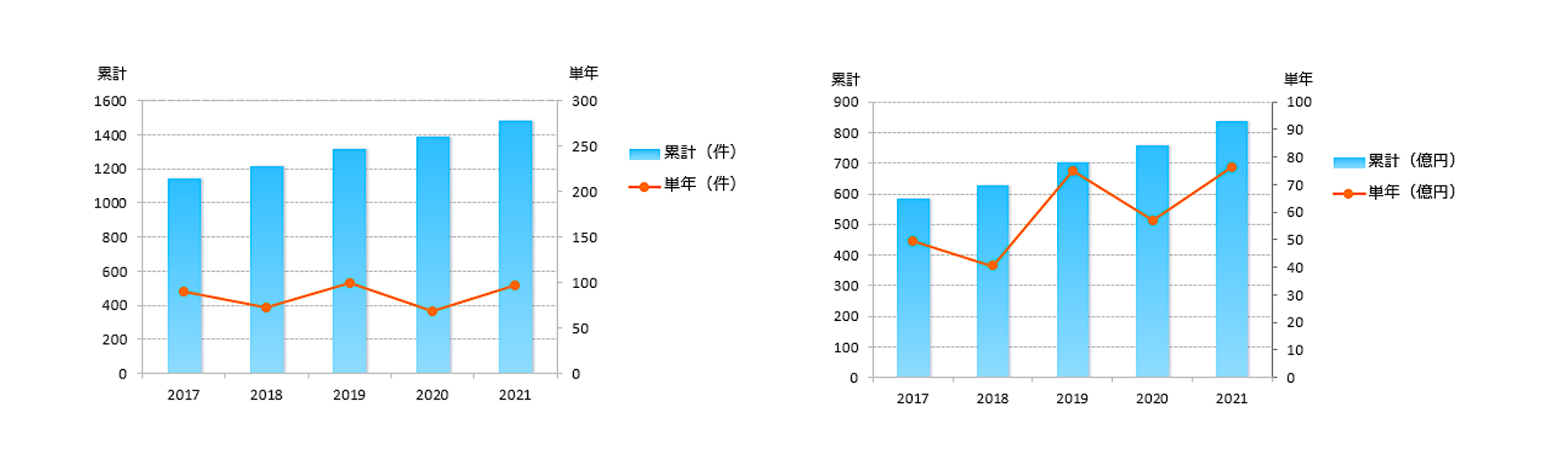

MUCAPの設立は1974年なので、48年もの期間に亘ってベンチャー投資を行っています。現在の三菱UFJキャピタルとなった2005年度以降、件数では1,400件超、金額でも800億円を超える投資実績(2022年5月末現在)となっています。これは恐らく、VCとして投資件数、投資先の上場件数において日本でトップクラスだと思います。ここ数年も、年間90-100件の投資を継続して実行しています。

- 三菱UFJフィナンシャルグループ(MUFG)におけるMUCAPの位置づけはどのようなものでしょうか。

MUCAPは、MUFGグループの中のベンチャーキャピタルです。運営するファンドは三菱UFJ銀行との二人組合ですが、一般的なCVCとは異なり、様々な領域・ステージのスタートアップ企業を積極的に応援すべく、投資においては、基本的に独立した意思決定を行っています。

現在40数名のキャピタリストがいます。銀行本体からの出向・転籍者と私のような外部からの中途採用者とが2:1ぐらいの人員構成です。

投資先へのバリューアップ支援においては、必要に応じて銀行・信託や証券のグループのネットワークや、知見を活かした支援や、営業面での協力など、幅広い支援を行っています。

- 投資領域や、投資ステージ、会社としてのスタンスなども伺えますか?

日本の銀行系VCとして、スタートアップ&ベンチャー業界を広く支援し、成長に寄与していくことをミッションとして掲げています。ライフサイエンス領域専門ファンド(100億円規模)も運用していますが、当社は特定の領域に偏るということはありません。また、ステージについても、シード、アーリーからレイターまで広くカバーしています。1社あたりの投資金額は1000万円〜5億円が中心のレンジとなっています。

投資検討期間は2ヶ月〜4ヶ月が標準的ですが、意思決定までには十分なディスカッション、コミュニケーションを重ねることを心がけています。特にスタートアップにおいては経営者、経営チームがカギとなることが多く株主として参画するにあたり、価値観への共感や、相性面などを確認することも大切です。ファイナンスニーズが顕在化し、数カ月後の着金をお願いしたいというタイミングより、カジュアルに意見交換できるタイミングで接点を持たせて頂けた方が結果的にスムーズに進むことも多いです。

- 一貫して在籍してきた理由、MUCAPだからこそ、といえる強みについても教えてください。

当社の強みは、日本において長年VC活動をコンスタントに続けてきた事、またそこから来る豊富な経験・知見だと思います。

長期的にコミットしてきた歴史でも明らかですが、外部環境の変化があっても、ベンチャー支援を続ける姿勢がブレることはありません。先ほども触れましたが、リーマンショック後の不況下においてすら、年間50件近い投資を続けていました。投資姿勢を変えることなく、スタートアップの経営陣と長期的な信頼関係を築いていけるという安心感は強みの一つだろうと思います。

また数多くの上場案件を支援してきた実績から、上場前後の時期における留意点や、最新の動向、対処するためのノウハウなど、数多くの事例からの経験則やナレッジを提供できます。

バリューアップ面の支援では、MUFGグループの幅広いネットワークを活用した支援にも特徴はあります。MUFGグループの取引先を営業先として紹介したり、融資部門との繋ぎ込みなどですね。

- 田口さんは、若い時分からベンチャー企業を支援する仕事に興味を持たれていたと伺いましたが、何かきっかけがあったのでしょうか。田口さんが学生だった時分(1990年代後半)は、VCは今ほど一般的ではなかったのではと思います。

「ベンチャーキャピタル」という仕事の存在を知り、具体的に興味を持つようになったのは学生時代に就職活動をするようになってからですが、成長や、挑戦をしていく人を支援するような仕事をしたい、という漠然としたイメージはもっと若い頃からありました。

中学、高校時代のころ、マッキンゼーの大前研一さん、ボストンコンサルティングの堀紘一さんのことをTVなどのメディアを通じて知り、本も好きでよく読んでいました。企業の経営や、成長戦略の助言をするコンサルティングファームという存在を知って、こういう仕事は面白そうだなぁ、と思っていました。

- 中高時代はどのように過ごされていたのでしょうか?

当時は、千葉の松戸に住んでいました。東京へのアクセスは悪くはないですが、ザリガニ釣りをする場所に困らない、のどかな田舎という感じの場所でしたね。全国的に「学校が荒れている」ことが社会問題になっているような時代だったのですが、私の中学校はそのサンプルのような学校だったように思います(笑)。

今では考えられないと思いますが、教師が生徒に対して暴力で押さえつける行為を目にするのは日常でしたし、校庭にバイクが侵入してきて窓ガラスが割られる、なんてことも時々ありました。私は水泳部に所属していたのですが、当時の体育系部活で、真冬の寒中水泳など当たり前で、ある意味心身ともに鍛えられたとは思っています。

- 尾崎豊の歌のような、すごい環境ですね。

高校は県立の進学校に進みました。中学校とは一転して、自由な校風で、制服もなく、個性が尊重される環境でした。運動部は中学でやり切ったという感覚もあったので高校では軽音楽部に入って、ギターを弾いていました。軽音楽部の大先輩に「爆風スランプ」のお2人がいる部活で、仲間と音楽を楽しんでいました。

早稲田大学に入ってからは、スポーツやアルバイト等学生生活を楽しんでいましたが、入った会計のゼミが真面目に勉強するところだったので簿記・会計は勉強しました。

- 新卒では、コンサルティングファームに入られましたが、就職活動における、考え、こだわりなどはあったのでしょうか。

人や企業の成長をサポートするという仕事にはもともと関心はあったのですが、明確に志望先になったのは、就職活動の中でちゃんと調べるようになってからですね。

当時は、就職氷河期と呼ばれた時代で、従来の日本の大企業が採用数を絞り始める中、コンサルティングファームが就職先として存在感が増していたことも影響したと思います。

この時から、VCの仕事にも関心はあったんですが、当時、新卒採用を行っているベンチャーキャピタルは2社しかありませんでした。将来的にベンチャー支援の部署への配属する話をいただいた上で、コンサルティングを体系的に学ぼうと、前職の会社に入社しました。その後4年目で今のベンチャーキャピタルに転職しました。

- 当時から「ベンチャー支援」に惹かれていた理由はどこにあったのですか?

「新しい価値の創造」や「飛躍・挑戦」の支援をしたい、という思いですね。

就活の中で調べるうちに、コンサルティングファームのクライアントは大企業が中心で、「生産性改善」「コスト効率の向上」等の切り口がどうしても多くなると分かってきました。コンサルティングファームを雇う体力のある企業はベンチャーには少ないので、構造的に仕方ないんだと。

その中で、フィービジネスではなく、「投資」という関わり方で支援できるVCという仕事を知り、非常に魅力的に映りました。

- 学生時代から、明確な仕事観を持たれていたんですね。メーカー、金融、商社など、日本の人気企業に興味は湧かなかったのですか?

あまり関心がなかったんです。一つは父親の影響かなと思うのですが、父は建築系の工事会社で、購買業務などの仕事に携わり、その部署で長く働いていました。すごく真面目な父で、家族のために働くというスタンスが明確な人でした。一方で、仕事そのものは全く好きじゃないことがありありと分かる人でした。「本当は他の仕事がやりたかったのに」という思いを抱えている父の姿を見ながら、「好きじゃない仕事をする」ことへの違和感や疑問を小さな頃から持っていた気がします。

学生時代、ある大手メーカーの金融子会社でアルバイトをしていたとき、その会社の方たちからも「モノづくりが好きで就職したのに、好きじゃない金融の仕事をさせられている」という人がほとんどで、自分の中で、父から感じたのと似た違和感を覚えていました。

そういった経験もあって、自分が就職先を考えるに際しては、志望する仕事にストレートに携われることが重要、という思いが明確にありましたね。

「やりたいと思う仕事に就けない可能性」を極力減らすことが一番の優先順位だったので、「経験の幅を広げるために入社後、様々な部門に配属される」ということが珍しくない日本の大企業は、就職先の選択肢として最初から入らなかったんです。

- やりたい仕事を突き詰め、現・MUCAPでのキャピタリストに辿りつかれた。理想の仕事にたどり着いた参画当初はどんな感じでしたか?

「将来性のある魅力的な会社に投資をして、しっかりバックアップをしていこう!」

という前のめりの思いはありつつも、仕事を始めるとすぐに「やりたいこと」と「できること」のギャップの大きさに直面しました。

業界のネットワークも、支援先の上場実績もない自分が「良いベンチャー」から選ばれるわけはなく、投資先の候補を発掘するだけで苦労しました。

同様に、社内的にも信用がないわけで、「これは!」という会社と出会えたとしても、社内を説得して投資の意思決定までもっていくことができない。事業の可能性や、調達金額、株価とのバランスについても考えなくてはいけないが、どう組み立ててよいかなかなかわからない。結果、自分からアプローチしたベンチャー経営者から期待をされ、数カ月間、コミュニケーションやDD対応をお願いしたにも関わらず、社内をまとめることができずゼロ回答になってしまう、そういう経験をしたときはその経営者に対して非常に申し訳なかったですし、つらかったですね。

ベンチャー企業と出会い、その企業の可能性や成功の蓋然性を検証し、納得性のあるストーリーに落とし込みながら、社内を巻き込み説得する。これがある程度できるようになる、までが一つ目の壁でした。

- VCやCVC業務に新たに携わるときに、誰しもが直面する「壁」じゃないかと思いますが、田口さんはどのように乗り越えられたのでしょうか?

今思えば、そもそものファインディング活動量と、投資先について考える「思考の深さ」が足りなかったんだと思います。

お会いしているベンチャーの絶対数が足りなかったので、限られた企業数の中で私が良いと思っても、会社の投資目線を満たさないという面はあったと思います。

また経験がないとき、キャピタリストは、起業家やスタートアップ側の事業内容、エクイティストーリーをそのまま鵜呑みにして、社内に伝えるだけのメッセンジャーのようになりやすい。それだと、周りを巻き込んで、説得していくことは難しい。その会社のことを自分ゴトとして捉え、「どの部分が新しい価値で何が成功要因なのか、どうしたら成長が加速できるのか、改善すべきところはないか、どこをサポートすべきなのか」などを繰り返し考えることだと思います。

社内で承認が得られるストーリーを組み立てられることは、必要なスキルだと思います。その企業や事業について知識も興味もない人に、自分が信じるストーリーを伝え、ワクワクさせることができるか。リスクリターンのバランスを踏まえても価値ある投資だと納得してもらえるか。まずは、その企業、事業、経営者について深く知り、考えることに力を注ぐ必要があると思います。投資後に営業紹介等を行う上でも必要なスキルなので、承認を得るためのプロセスをサラリーマン的な「社内営業」だ、とネガティブに捉えるのは間違いだと思います。

- 起業家からも社内からも信頼を獲得するためには、それくらいの努力が求められるということですね

そういうことが当たり前にできるようになったときに、次の視界が見えてきましたね。

スタートアップは経営者が8割

- 1つ目の壁を乗り越えた後に、出てきた新しい壁はどのようなものだったのでしょうか

二つ目の壁は、投資の承認を得られる納得性の高いストーリーを作りやすい投資先と、実際に成功する投資先、との間に、ある部分でギャップがあることに気づいたときでした。

投資検討の際、「大企業と取引関係があって技術的にも評価されている」ことや「有名大学の教授が技術顧問についていて、特許も取得している」といった事実は、ある種の安心材料になりますし、社内の説得にはプラスに働きます。ただ、その事実と、ベンチャー企業の成功とはあまり相関しない、ということに多く出くわしました。そのような情報は大いに参考になりますし、重要ではあるものの、その事業の成長を約束してくれるものではない。そんなことは当たり前ではあるのですが、「では、何に依拠してDDをし、何を信じてストーリーを構築すべきか」がわからなくなりました。

DDや社内の説得フェーズをある程度ハンドリングできるようになったが、上場やエグジットという成果につながらないという状況をどう打破すべきなのか。悩みましたね。

- 2つ目の壁は、さらに本質的で難しいですね。打開できたきっかけは何だったのでしょうか?

2009年のリーマンショックがターニングポイントでした。

金融危機下で、ベンチャー投資をするプレイヤーが激減するなか、規模の縮小は一部あったものの、MUCAPでは投資活動を続けることはできていました。投資先ソーシングにおける競争環境がほとんどなくなったため、この時に優れた起業家、ベンチャー企業と多くのご縁ができました。

未曽有の不景気ですから、ベンチャー企業も業績面では苦しくなるところが多いわけですが、不況下でもしっかりと生き残り、力強く新しい価値を生み出し、上場を果たしていくベンチャー企業がいる。対照的なコントラストが起きる現場に間近で遭遇しました。

そして、その差が「経営陣」にあることに気づいたんです。経営陣がしっかりしていると、採用で強く、顧客も応援してくれ、株主も巻き込んだファインナンスも実現でき、強い企業に育っていく。成功していく経営陣を実際に見させてもらったことで、自分なりの目線が出来てきたように思います。

この気づきを得て以降、ベンチャー投資に取り組むに際してのモノの見方、考え方、捉え方が大きく変わるようになりました。自分にとってすごく大きな財産ですね。今では、「スタートアップの成功は、経営陣で8割近く決まる」というのが実感です。

- 田口さんが感じる「成功する起業家、ベンチャー経営者」の条件を、あえて言語化するとどういうものになりますか。また、どのようにそれを感じるのでしょう?

タイプや得意分野などは千差万別ではありますが、巻き込み力、馬力は総じて高い印象です。また、事業や組織のことをどこまでも深く考えられる人が多い印象です。

そういった資質を感じ取るためにも、コミュニケーションをしっかりと取る。色々な場面で、様々な質問や話をしますね。何を実現していきたいか、ということもそうですが、一つのモノゴトの判断プロセスについての質問や、過去に上手くいかなかったときの失敗体験なども聞くようにしています。

巻き込み力の高い人は支援者が集まってきますので、そういうやり取りをできる関係を築いていくうちに、私自身もその経営陣、会社を応援したい気持ちになっていきます。

事業会社・CVCとスタートアップ連携の成功パターン

- 変化の激しい世界で、20年以上キャピタリストを続けられています。「やりたい」という思いだけでは、実現できないと思いますが、心がけていることなどありますか?

一つは自分の興味関心を持ち続けられる分野を作ること。

その上で、規模や、時間軸、ビジネスモデルなどのバランスも気にしながら投資先を見出していくということでしょうか。

自分の場合は、興味領域を大きく2つに区切り、既存の産業をDXで変革するBtoBの分野と、新しいエンターテイメントやコンテンツ・メディア等BtoCの分野がだいたい1:1になるように意識しています。

ベンチャー投資の難しい要素として、時系列的に成功より失敗が先に判明するというのがあると思います。事業の展開がうまくいかず資金に詰まったり、業績が伸びずに減損処理を行うことになったりということは、ベンチャーに関わっていればよくある話です。そういうことを気にしすぎたりするのではなく、金額の規模を抑えるなどしながら、とにかく実際に投資をして経験を積んでいくことが大切なんだろうと思います。

私も自分の過去を振り返って、もっと数多く挑戦すればよかったと思っています。

- キャピタリストに求められる資質のようなものはありますか?

私見ですが、資質という意味では、「好奇心」は求められると思います。

最近はWeb3.0などが話題ですが、そうした新しい技術やトレンドについては国内外の記事や、イベントに参加したり、人に聴いたりなど情報収集は欠かさないです。新しい分野に関しては、自分より若い人たちのほうが詳しいことは当然多いですが、歳の差など気にせずどんどん教えてもらうようにしてます。

そういうことが苦痛な方にはお勧めできない仕事でしょうね。

私の場合、つらい時期や苦しい時期はありましたが、この仕事に就いてから「もう辞めたい」と思ったことは一度も無いです。経験を積んで、最近の方が良い案件と巡り会えることが増えてきて、若い時より仕事をする時間も増えているくらいです(笑)。新しいものが好きですし、人が好きなんだと思います。

変化についていくキャピタリストであり続けるために意識しているところですね。

- 田口さんの今後の目標などはありますか?

メガバンクとベンチャー企業という異なるカルチャーの間(はざま)に位置するという面でも、ユニークな職場と感じています。

そういった環境において、キャピタリストとしての活動を長く続け、新しいチャレンジをし、出来る事を増やし、知見を磨きながら、”銀行系キャピタリスト”として、若手に少しでも良い影響を与えられるようなロールモデルになれたらと思っています。

- ここ数年、事業会社もCVCを通じたスタートアップ投資に活発になっています。世の中を良くするベンチャーの成長支援していくという面で、事業会社系のCVCに期待すること、連携できることはありますか?

いわゆる日本の大企業とベンチャー企業では、意思決定のスピード感、その考え方など、あらゆる面でカルチャーギャップがあるため、橋渡しを担うCVCの役割は大きいと思います。

CVCという難易度の高いプロジェクトで、事業面・投資面の両輪で成果につなげるには、トップダウンで長期コミットをしたうえで、スピーディに内部を巻き込み動かせる仕組みを用意していくことが求められると思いますね。

スタートアップにとって、大企業との連携を試みることの負荷は小さくないですし、機能する仕組みがない中で、推し進められると負の影響にもつながり得る。それでも、大企業が持っている顧客基盤や層の厚い人材プールなど、スタートアップの成長に寄与するポテンシャルが大きいことは間違いないと思います

スタートアップを支援するという同じ目線で考えた場合、事業会社系の株主に求められるものは主に二つだと感じます。

一つは、プロダクトの磨き上げへの助力。POCから一貫して誠実でスピーディなフィードバックがあり代表的な導入先になってもらい、それが水平展開のマーケティングにも使えるような事例を作っていってくれるというケース。

もう一つは、保有している強固な顧客基盤を活かして、商流における戦略的なパートナーとして機能してくれること。「代理店」という立場よりもっと踏み込んで、スタートアップのプロダクトが組み込まれた新しい商品サービスを作ってもらい、売り上げが伸びる仕組みを一緒に作ってくれる、というケースです。

我々の投資先でも、事業会社やCVCが株主になられたことで、大いに助かっているケースはこの二つのどちらかに該当しますね。

今後CVCとしての成功事例が増えていけば、事業会社の資金力とポテンシャルを活かしてスタートアップが成長し、世の中にも新しい価値が生まれていくという土壌が広がっていくのではとないかと思います。

CVCの活動が、大企業における一時的なオープンイノベーションや、新規事業開発への刺激というものにとどまらず、ベンチャー側にもメリットがあるようなっていけば心強いです。

- 最後に、今後出会っていきたい起業家像や、スタートアップが果たすべき役割について、田口さんのお考えをお聞かせください。

抽象的ですが、応援したい気持ちになる経営者にお会いしたいです。

「世の中に良いインパクトを与える」という信念、強いこだわりのある方たちとの出会いはいつでも刺激的です。

産業においてスタートアップやベンチャー企業ならではの良さは、スピード感やその突破力にあると思います。事業において「ゼロイチ」をやって成功するのは大変ですし、やること自体に大きな勇気がいる。

東京大学の入学式で起業の話が出るようになるなど、人生の大きな選択肢の一つとして、「起業」が位置付けられるようになってきた現状に期待していますし、これからも新しい会社や素晴らしい経営者と出会っていけることを期待し、楽しみにしながら、キャピタリストを続けていきたいと思っています。